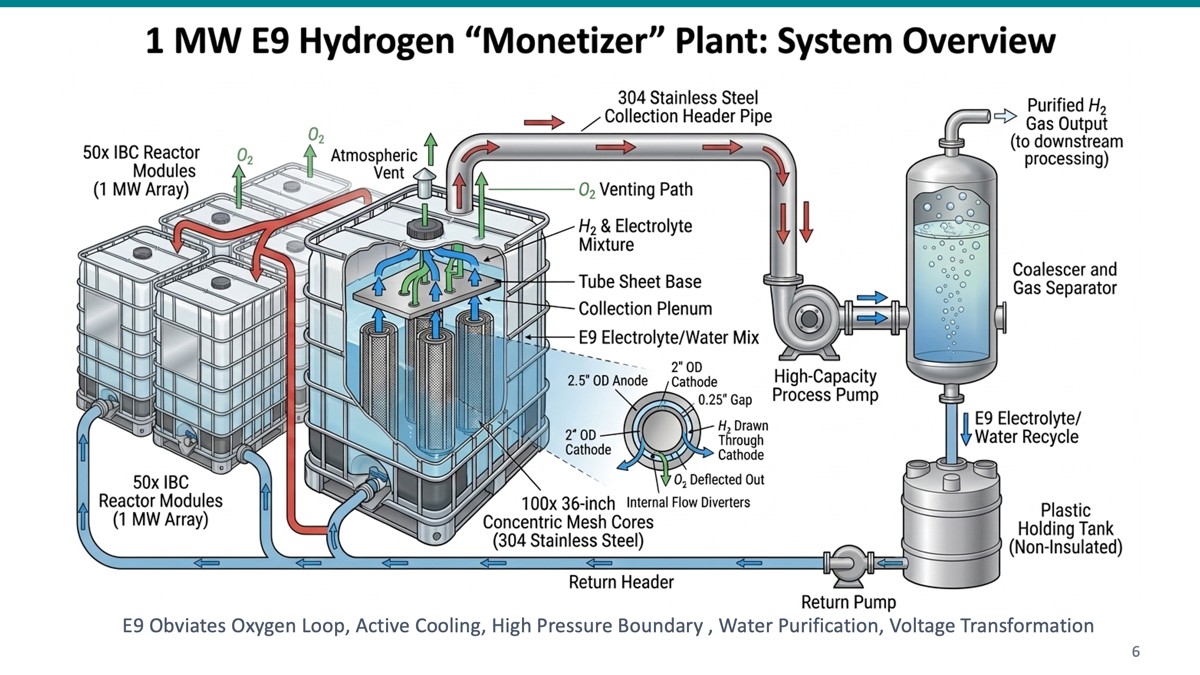

The Hydrogen Monetizer

One Platform. Both Problems. Solved.

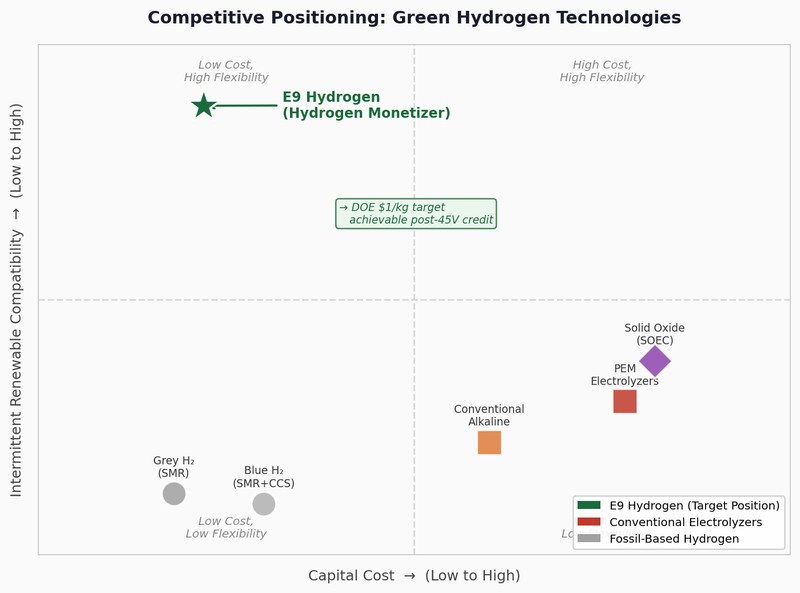

E9 Hydrogen deploys turn-key, zero-capital-to-host electrolyzer systems behind the meter at renewable projects — capturing wasted energy and converting it into green hydrogen at near-zero feedstock cost.

Zero-Cost Feedstock

Systems operate during curtailment and negative-pricing windows, achieving median feedstock costs of –$17/MWh — a structural advantage of $37–90/MWh versus dedicated projects.

Zero Capital to the Host Site

E9 owns and operates the equipment. The renewable project contributes only space and surplus power. New revenue begins flowing with no capital outlay required from the host.

Turnkey Energy-as-a-Service

Delivered as an EaaS partnership with a Strategic Solutions Partner (SSP), covering CAPEX, technical integration, NFPA 2 safety compliance, and full commodity offtake and logistics.

Subsidy-Independent Economics

Financial model excludes 45V production tax credits — viability is built on commodity sales, low feedstock costs, grid services, and resilience revenue. Federal policy shifts don't break the model.

How the Monetizer Works

A 20 MW deployment, illustrative economics

1

Your renewable project generates surplus power — wind, solar, or off-grid capacity that cannot reach the grid or would be curtailed.

2

The E9 electrolyzer activates in seconds — direct DC coupling enables cold starts that capture even short curtailment windows that PEM systems miss.

3

The electrolyzer produces green H₂ — ~850 MT per year from a 20 MW deployment at 29% capacity factor.

4

SSP aggregates & routes H₂ — to industrial offtakers, transport networks, or conversion into green ammonia or e-methanol for global commodity markets.

5

Revenue flows to all participants — $1.7–$3.4M+ additional annual revenue to the host site at $3–$5/kg net of OPEX. Payback: 3.5–7 years.